Under Internal Revenue Code (IRC) Section 280E, cannabis businesses are historically prohibited from deducting ordinary business expenses – such as rent, payroll, and marketing – from their federal taxes. This is because the plant remains classified as a Schedule I controlled substance. Many states simply reflect federal tax policy in their own tax codes; thus, cannabis businesses in those jurisdictions are also blocked from state-level tax deductions. As a result, many cannabis businesses are estimated to pay effective tax rates of up to 50% or more.

Colorado became the first state to approve 280E deductions in 2014. In 2016-2021, Arkansas (2019), California (2019), Hawaii (2016), Louisiana (2019), Minnesota (2019), Michigan (2019), Maine (2018), Montana (2017), New Mexico (2021), and Oregon (2016) approved laws to exempt, or “decouple”, businesses from Section 280E. In 2022, Illinois, Maryland, Massachusetts, Mississippi, Missouri and Vermont permitted 280E deductions for their cannabis industry. In spring 2023, Connecticut, Delaware, New Jersey, New York, Virginia and Washington DC passed similar legislation that allows cannabis companies to deduct business expenses from their state income taxes.

By early 2026, the list of decoupled jurisdictions has grown to include Rhode Island, Ohio, Pennsylvania, Alaska, and Nevada, while Arizona is currently finalizing legislation to align its state tax code with a potential federal Schedule III status. As of April 2026, 28 U.S. states and Washington D.C. have decoupled IRC 280E from their state tax codes.

The scope of relief continues to vary by geography: some states allow deductions for both corporate business tax and personal/gross income tax (benefiting pass-through entities like LLCs), while others restrict these deductions to C-corporations only.

Effective April 22, 2026, the federal government officially moved medical cannabis to Schedule III. Here is the current status:

- Medical Cannabis: Now in Schedule III. These businesses are exempt from Section 280E and can now deduct normal operating expenses from their federal taxes.

- Adult-Use (Recreational) Cannabis: Remains in Schedule I. These businesses are still subject to 280E restrictions and cannot yet claim federal tax deductions.

- Key Date: An administrative hearing is set for June 29, 2026, to decide on moving adult-use cannabis to Schedule III as well.

Even with these federal changes, state-level “decoupling” remains a factor. Businesses in states with “static” tax codes that do not automatically update with federal law may still face local tax barriers until those states pass specific legislation.

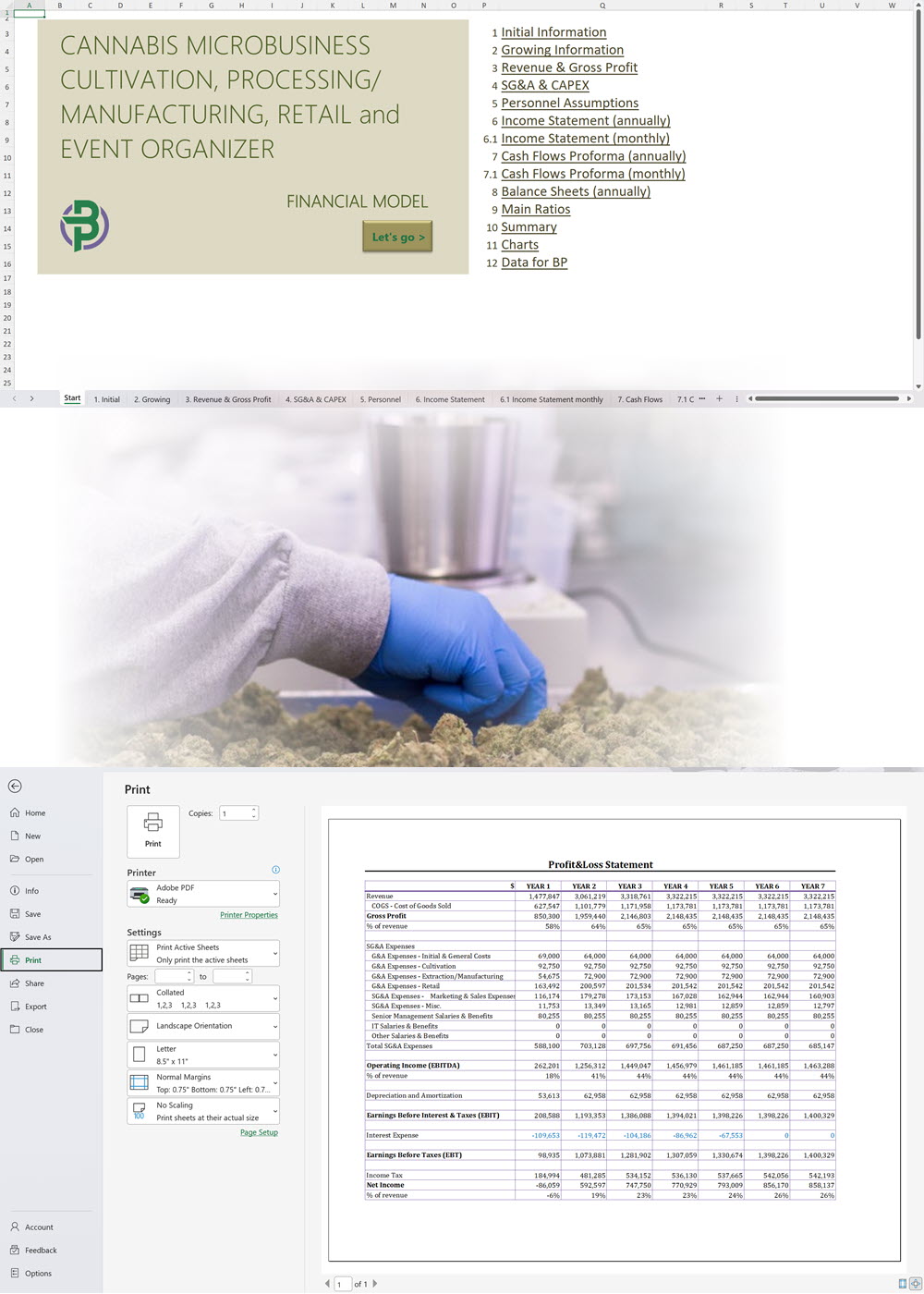

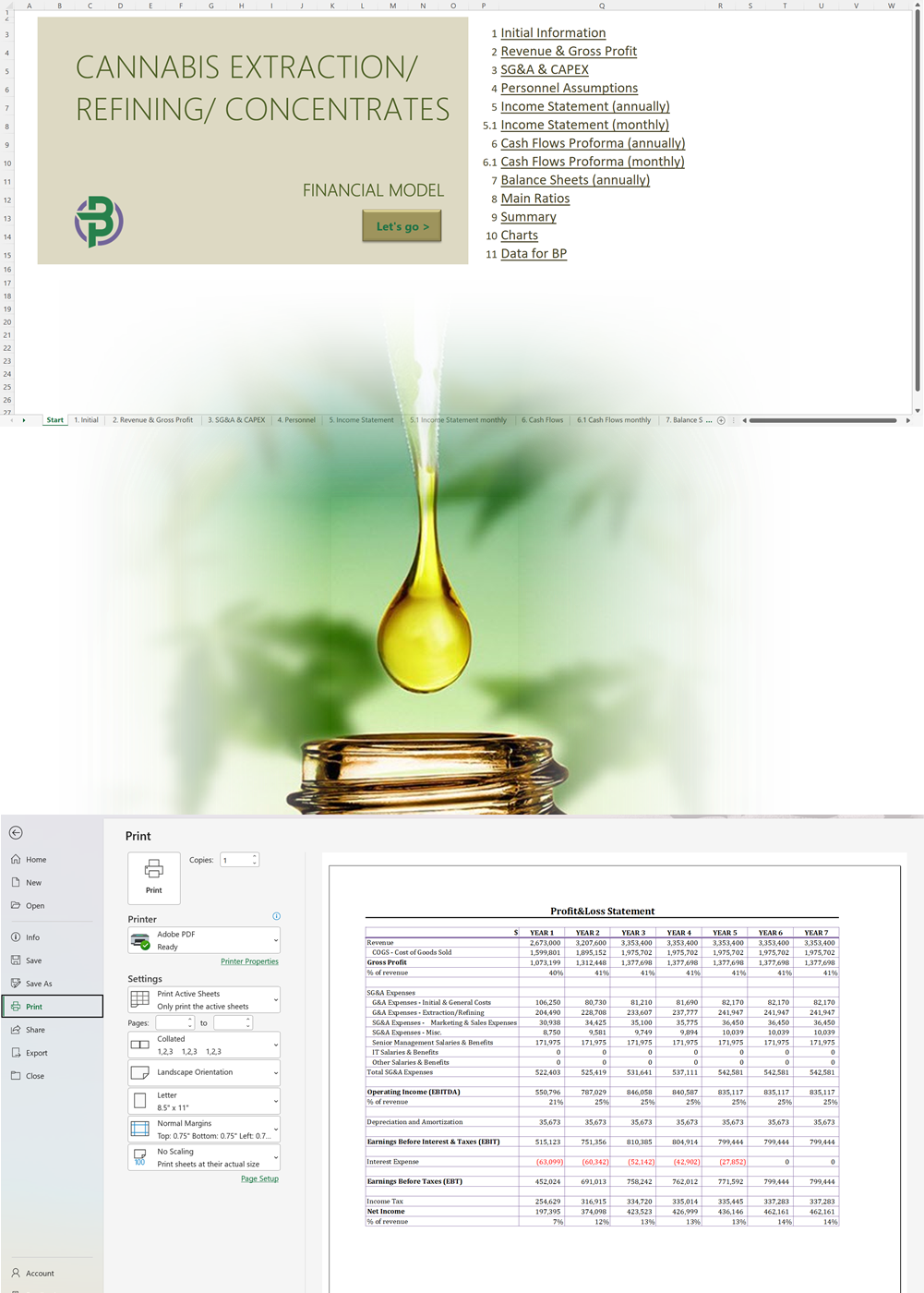

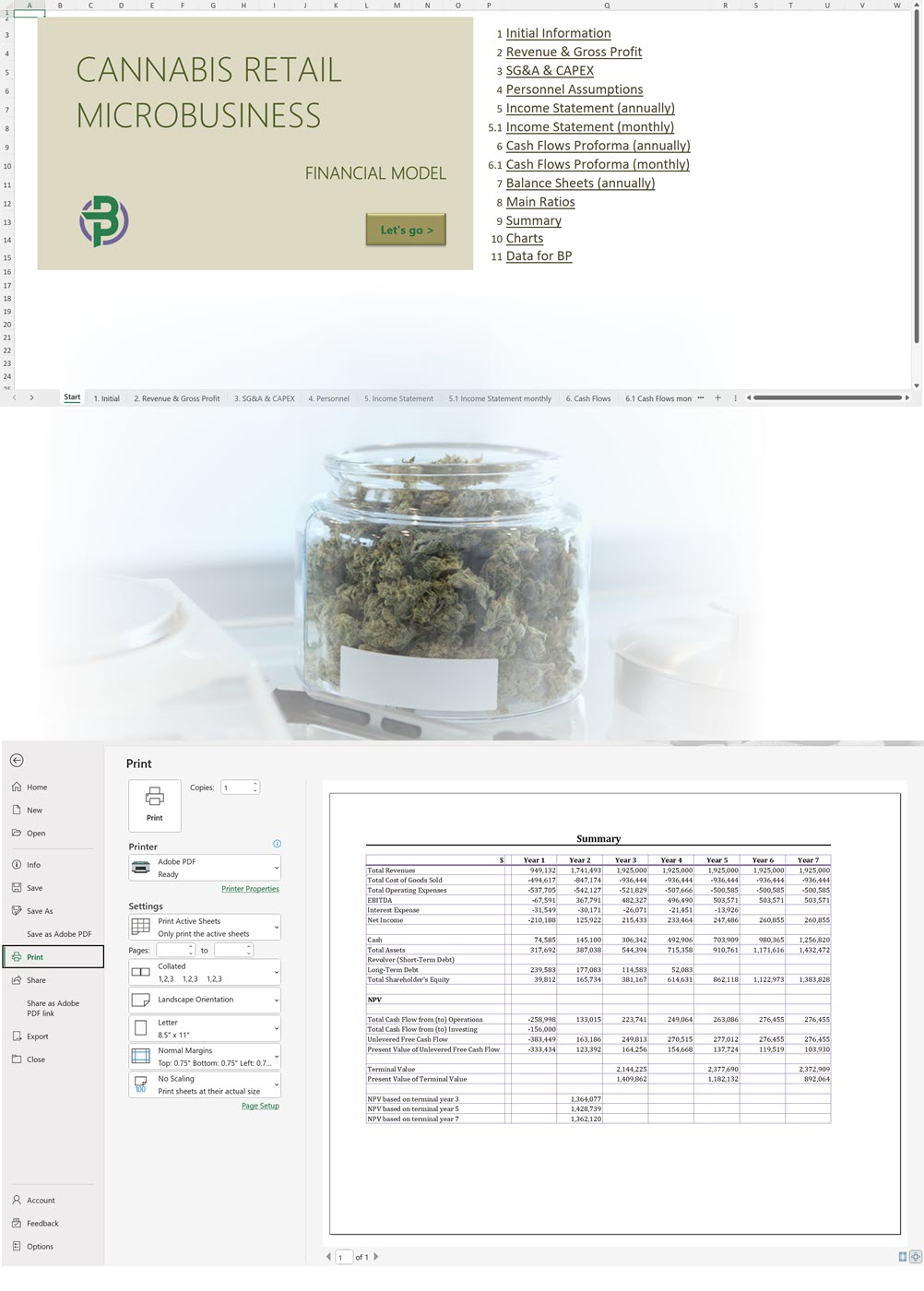

Retail Cannabis Business 280E Deductions Sample, Year 7 (New Jersey)

| under the Section 280E | state-level exemption | |

| Revenue | 3,300,000 | 3,300,000 |

| GOGS | 1,431,255 | 1,431,255 |

| Gross Profit | 1,868,645 | 1,868,645 |

| SG&A Expenses | 561,733 | 561,733 |

| Operating Income (EBITDA) | 1,306,972 | 1,306,972 |

| Depreciation and Amortization | 19,500 | 19,500 |

| Earnings Before Interest & Taxes (EBIT) | 1,287,472 | 1,287,472 |

| Interest Expense | 0 | 0 |

| Earnings Before Taxes (EBT) | 1,287,472 | 1,287,472 |

| Income Tax | 560,624 | 508,309 |

| Effective Tax Rate | 43.5% | 39.5% |

| Net Income | 726,848 | 779,163 |

| % of revenue | 22% | 24% |

| Ending Period Cash | 3,990,741 | 4,381,519 |

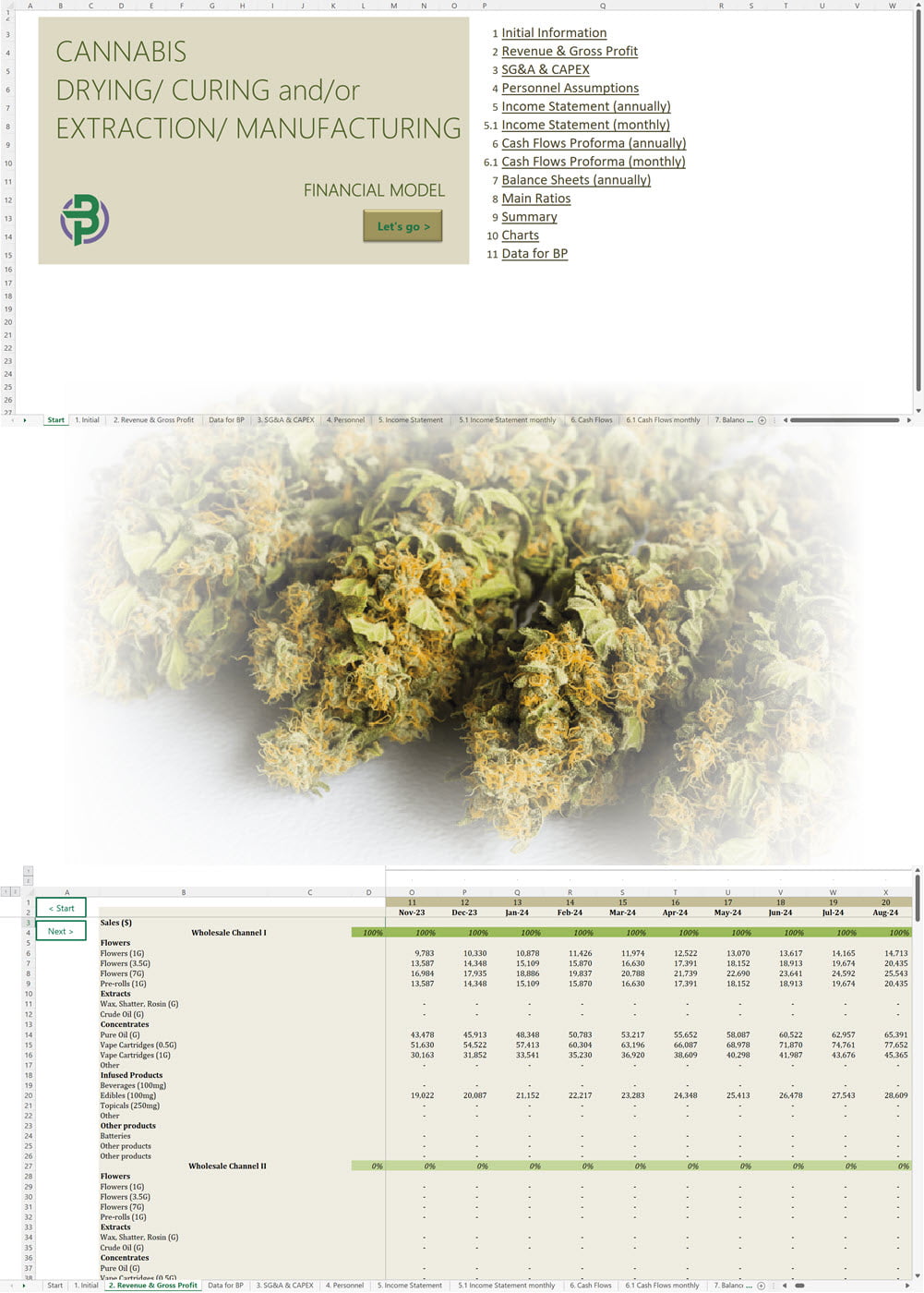

'70% ready to go' business plan templates

Our cannabis financial models and cannabis business plan templates will help you estimate how much it costs to start and operate your own cannabis business, to build all revenue and cost line-items monthly over a flexible seven year period, and then summarize the monthly results into quarters and years for an easy view into the various time periods. We also offer investor pitch deck templates.

Best Selling Templates

-

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00 Select options This product has multiple variants. The options may be chosen on the product page -

Cannabis Dispensary Investor Pitch Deck Template

$75.00 Select options This product has multiple variants. The options may be chosen on the product page -

Cannabis Financial Model All in One

$250.00 Select options This product has multiple variants. The options may be chosen on the product page

Hemp CBD business plan templates are available at hempcbdbusinessplans.com.

Our Templates

Cannabis Retail Business Plan Template (with or without Delivery)

Price range: $75.00 through $350.00

Cannabis Retail Microbusiness Business Plan Template

Price range: $75.00 through $275.00

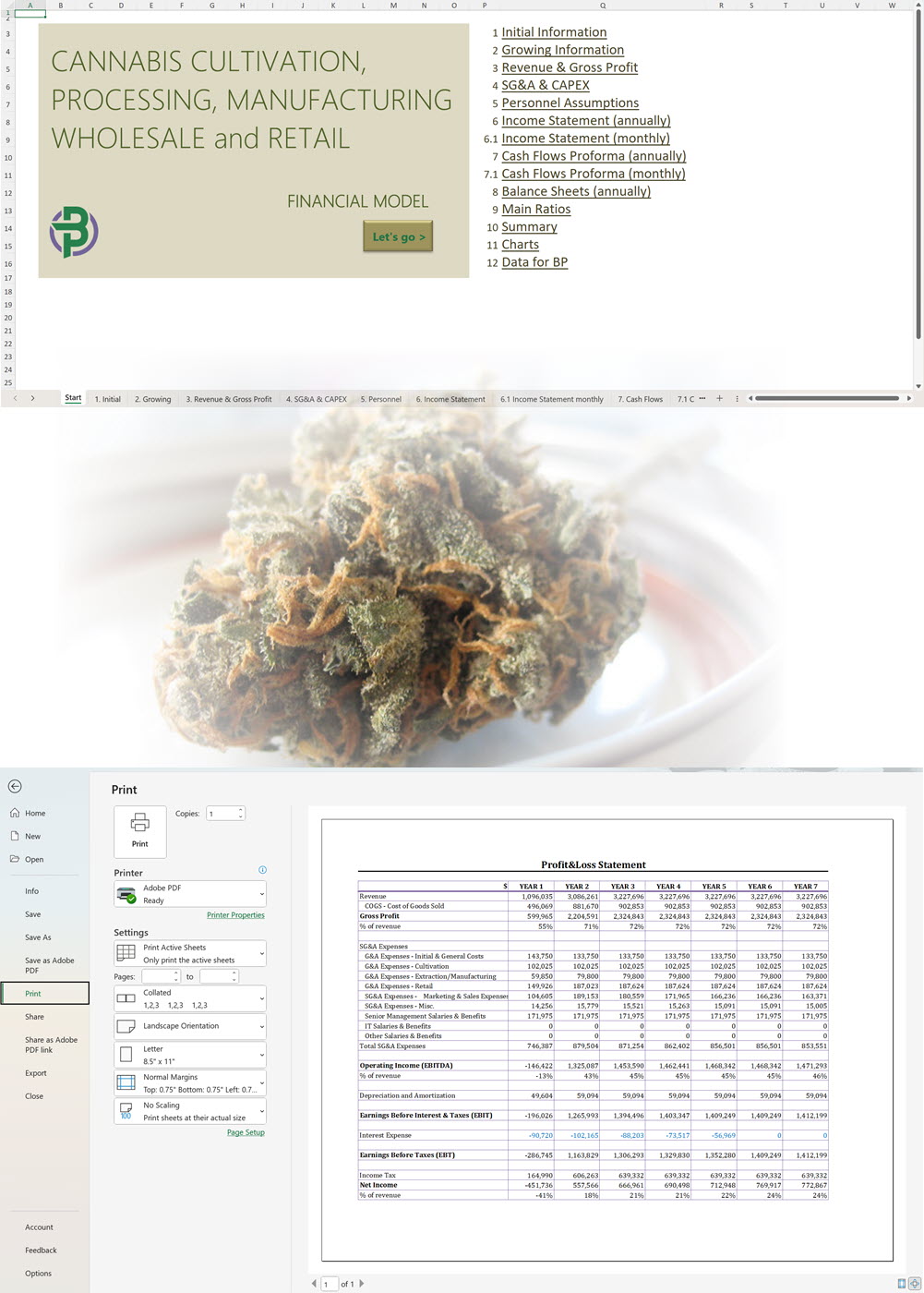

Cannabis Cultivation, Extraction, Manufacturing, Distribution, Retail and Microbusiness Business Plan Template

Price range: $75.00 through $500.00

Cannabis Micro Cultivation Business Plan Template

Price range: $75.00 through $300.00

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00

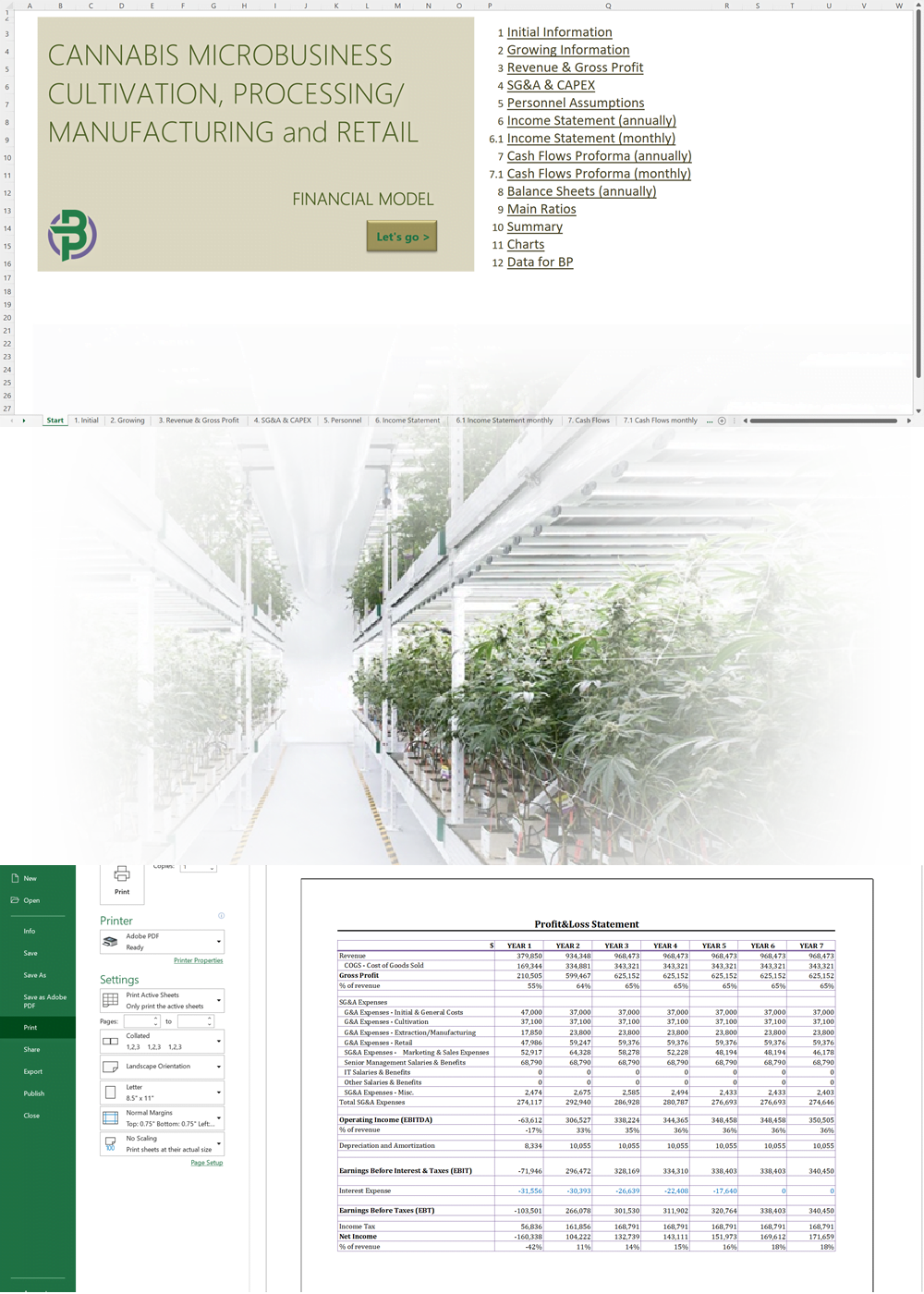

Cannabis Microbusiness Cultivation and Manufacturing Business Plan Template

Price range: $75.00 through $350.00

Vertically Integrated Cannabis Business Plan Template

Price range: $75.00 through $500.00

Cannabis Microbusiness Business Plan Template for Cultivation + Extraction + Manufacturing + Wholesale + Retail + Services

Price range: $75.00 through $500.00

Cannabis Transportation Business Plan Template

Price range: $75.00 through $275.00

Cannabis Cultivation, Extraction and Manufacturing Business Plan Template

Price range: $75.00 through $450.00